This article maps the landscape of ESG in concept, outlines political arguments, summarizes recently passed bills nationally and will leave you with 5 key takeaways to support a meaningful dialogue with both sides of the aisle.

Written by

Sara Hickman, LEED AP, WELL AP

Senior Vice President, ESG Lead

At its core, ESG is a means of risk identification and evaluation for financial and non-financial issues.

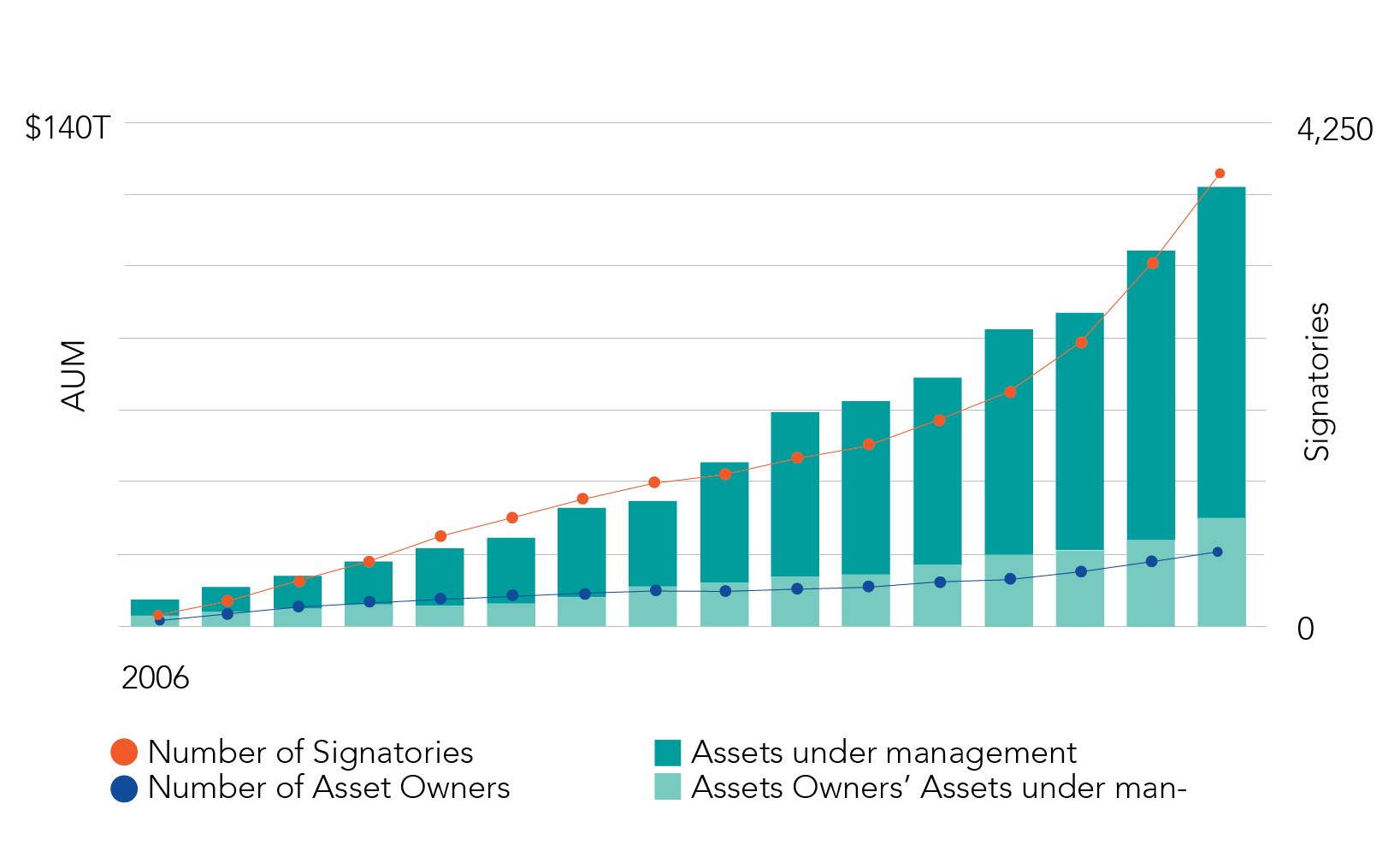

GRESB and UNPRI are most widely adopted and rapidly growing ESG reporting standards in commercial real estate.

We’ve been preaching the triple bottom line for decades. ESG is a reformatting of this approach. A means of risk identification and evaluation for financial and non-financial issues, ESG investing is implemented through one of three approaches:

Investors are increasingly expecting more than yields from their investments. These investors require competitive returns with assurances that companies are keeping their promises.

“Investors recognize that solving the climate crisis is one of the biggest challenges of this decade. Flows into ESG funds doubled from 2020 to 2021. That trend is poised to continue in the coming years, predicting that ESG assets will hit $30 trillion by 2030.”

“We are seeing investors globally embracing ESG investing at a staggering rate and are expecting an increase to 21.5% of total assets or $33.9T by 2026.” (PWC)

Organizations aligning their business strategies with ESG criteria signal to their shareholders they are “walking the talk” by taking actions that are consistent with their values. As “greenwashing” becomes an increasingly dirty word in the investor’s vernacular, organizations that cannot back up their claims with reliable data risk losing out in the long-term.

As the anti-ESG arguments and bills continue to pile up, we have found 4 common themes across anti-ESG bills, and naturally have our own response (from an investment perspective, we assure you).

Market inefficiency: ESG investing is not based on sound economic principles, leading to market inefficiency because of prioritizing social and environmental factors over financial considerations.

Cost: It is too costly for companies to implement and may lead to reduced profits or higher prices for consumers.

Ideological bias: ESG policies are based on a left-leaning ideological bias, pushed by politicians and activists with an agenda.

Limited impact: ESG investing has limited impact on the environment or social issues distracting from more effective solutions.

Ultimately, investors and policymakers who understand ESG considerations are important for long-term sustainability and financial performance will realize the benefits.

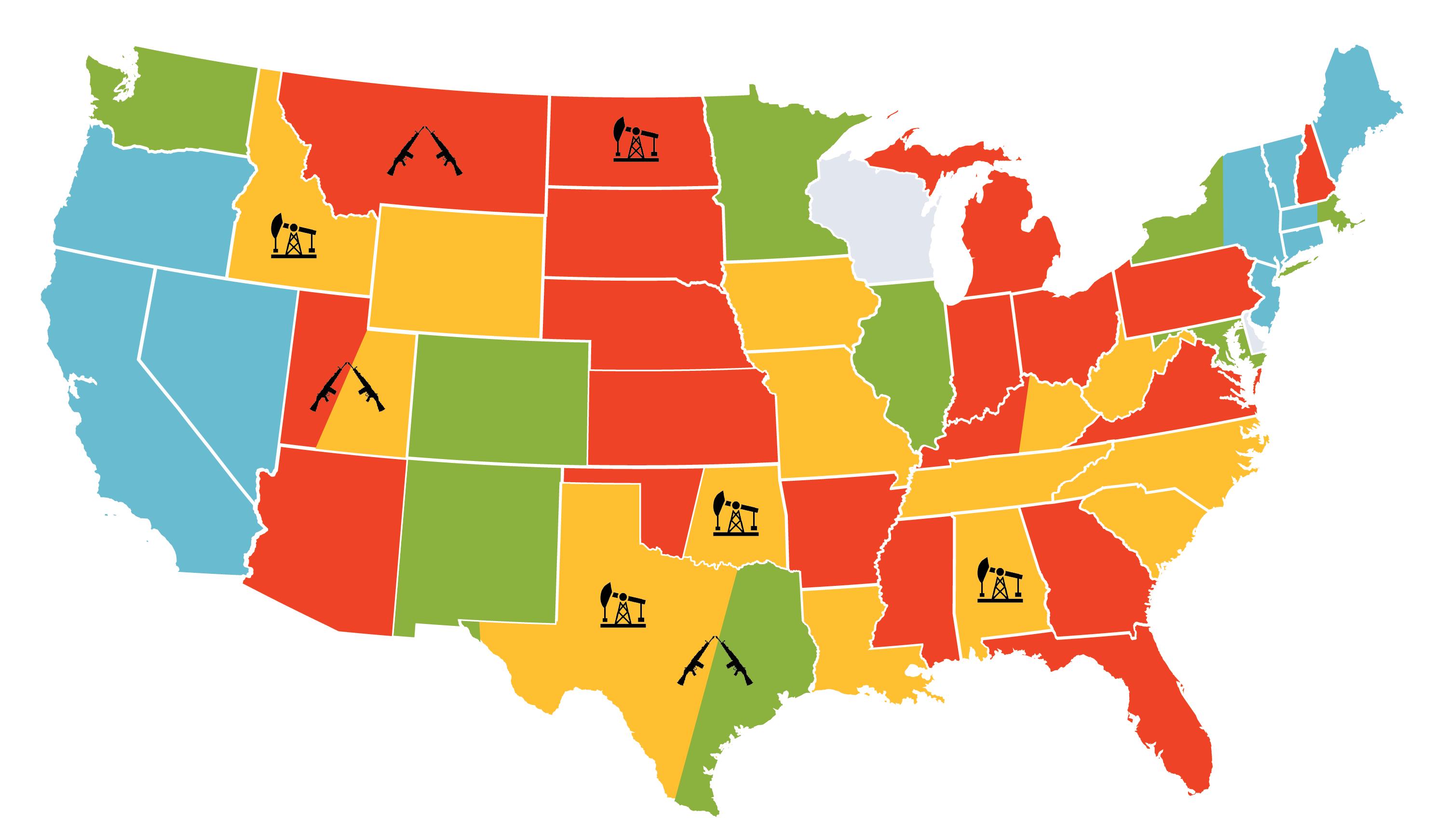

The red wave has come forth with vengeance, pushing back against ESG investing through state pension funds. If you are an avid supporter of ESG, no doubt you’ve received your fair share of anti-ESG articles from your “right” minded colleagues. In my opinion, they were weak in the beginning, full of flashy headlines and editorial opinions which demonstrated an incomplete understanding of ESG at best; frequently shifting to pro-ESG arguments toward the end. Over the past several months, policy makers have generally pivoted away from full-blown attacks on ESG investing in response to staunch rejections from state legislators. Rejection leads to refinement, and lawmakers now have a new target: the elimination of investment firms that are anti-fossil fuels, arms and ammunition. The map below indicates passed ESG specific legislation since August, 2023 both pro and against.

Note, icons represent industries protected through anti-ESG bills.

Green I Promotion of ESG evaluations in investment decisions / Focus on climate change risks.

Blue | Promotion of divestment from fossil fuel and/or firearms/ammunition (not 100%) / Net Zero Carbon Pathways & Targets.

Red | Restriction of ESG considerations in investment decisions / Eliminates ESG requirements / protection of specific industries / minimizes ESG factors

Yellow | Targets entities that boycott fossil fuel / firearms / ammunitions / Eliminates firms who promote clear divestment

Source: Ropes & Gray

Let’s refer to Approach A as broad sweeping anti-ESG bills, which prohibit investment by state pension funds in firms that evaluate using ESG factors. Approach A has a low win rate. Such aggressive stances are consistently reported as “too costly to the state” bearing “too many unintended consequences”. Detractors also note that this approach is “inconsistent with the state’s fiduciary duty” and is “misleading”.

In contrast, Approach B denies investment firms that screen and filter out industries such as fossil fuels, firearms and ammunition. These bills are winning because they include clear and defined parameters.

What really matters here? Money of course. Florida has passed the most aggressive legislation against ESG for state pension funds (valued at $108B). For context, the following state pensions are valued as follows; Maryland ($64B), Massachusetts ($104B), Texas ($180B) and California ($750B).

And of course, California again leads the way by passing the Climate Corporate Data Accountability Act which will require greenhouse gas data disclosure for organizations with total annual revenues in excess of $1B that do business in California. Even if your company doesn’t hit that, your tenants or investors might. (Stay tuned for more.)

This is a simple case of action & reaction through the balancing act of two opposing political sides, keeping us in check. At the end of the day, whether ESG based or not, investing is fundamentally based on maximizing returns while minimizing risk. In an increasingly volatile market, does it really make sense to ignore specific risks based on political principles? We didn’t think so.

To learn more about ESG, contact Sara Hickman: [email protected] | 857.998.7911